Compass February 2026 National Real Estate Insights

A Slow Start to the Year – But Spring Momentum Is Building

The January sales statistics reflected in this month’s report capture the very slow holiday market of December and early January, the period when most of these offers were negotiated. Historically, January posts the lowest sales volume of the year along with some of the weakest standard measurements of demand.

For that reason, these figures have limited value as predictors of what the 2026 housing market will ultimately look like. As listing inventory and buyer activity begin to accelerate, we expect meaningful shifts in the data over the next month or two, offering a much clearer picture of market direction.

Last year’s spring market was notably impacted by the tariff shock, which dampened consumer confidence and slowed momentum. Barring any new economic disruptions, the upcoming spring market is positioned to be considerably stronger.

January by the Numbers

Nationally, the median house sales price ticked up slightly year over year, signaling continued price resilience despite softer activity. However, existing-home sales declined approximately 7%, with winter weather likely contributing to the slowdown in many regions.

Other key metrics include:

-

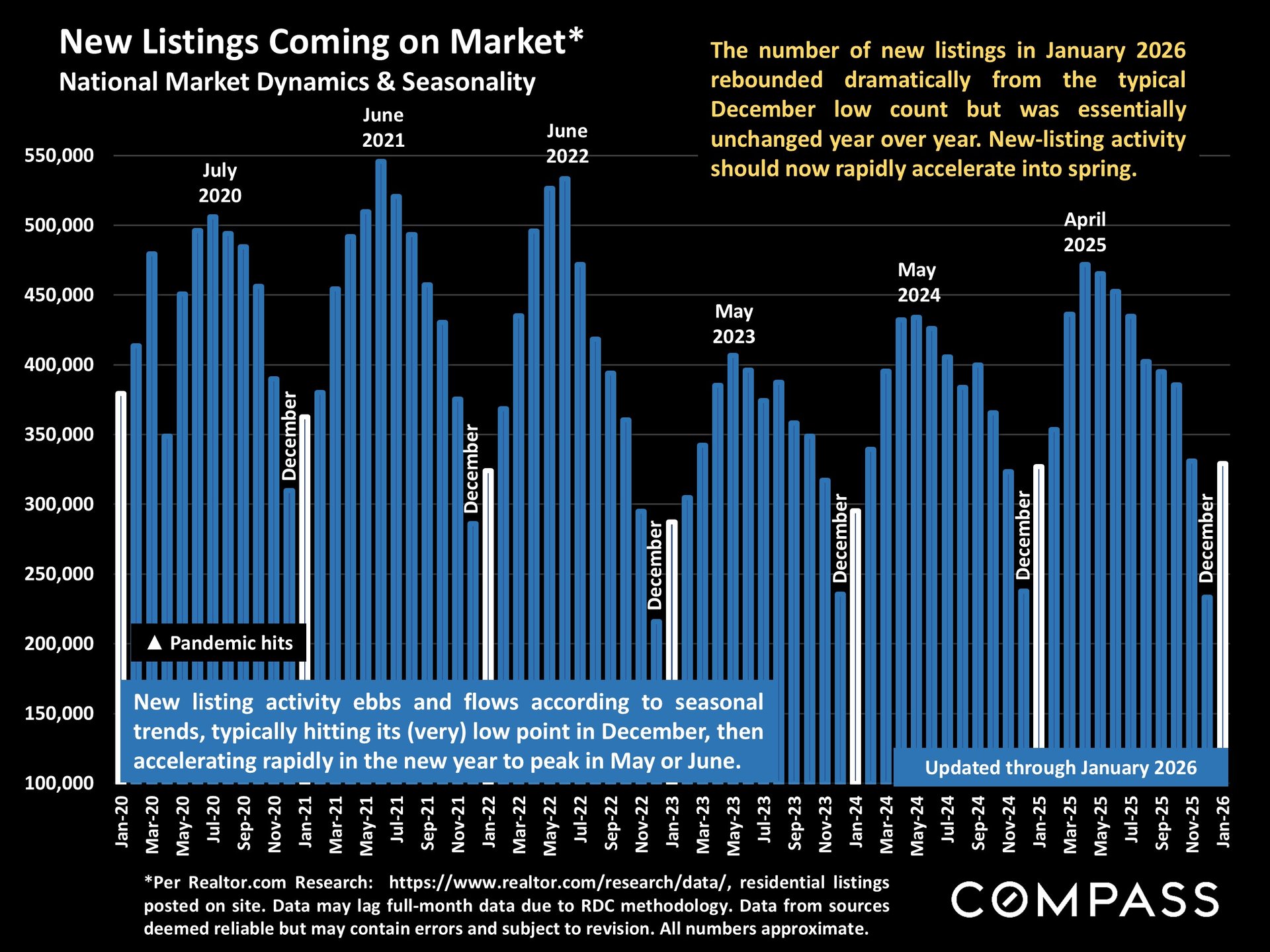

Listing supply: Up approximately 3.4% year over year

-

Median days on market: 46 days (up from 41 days in January 2025)

-

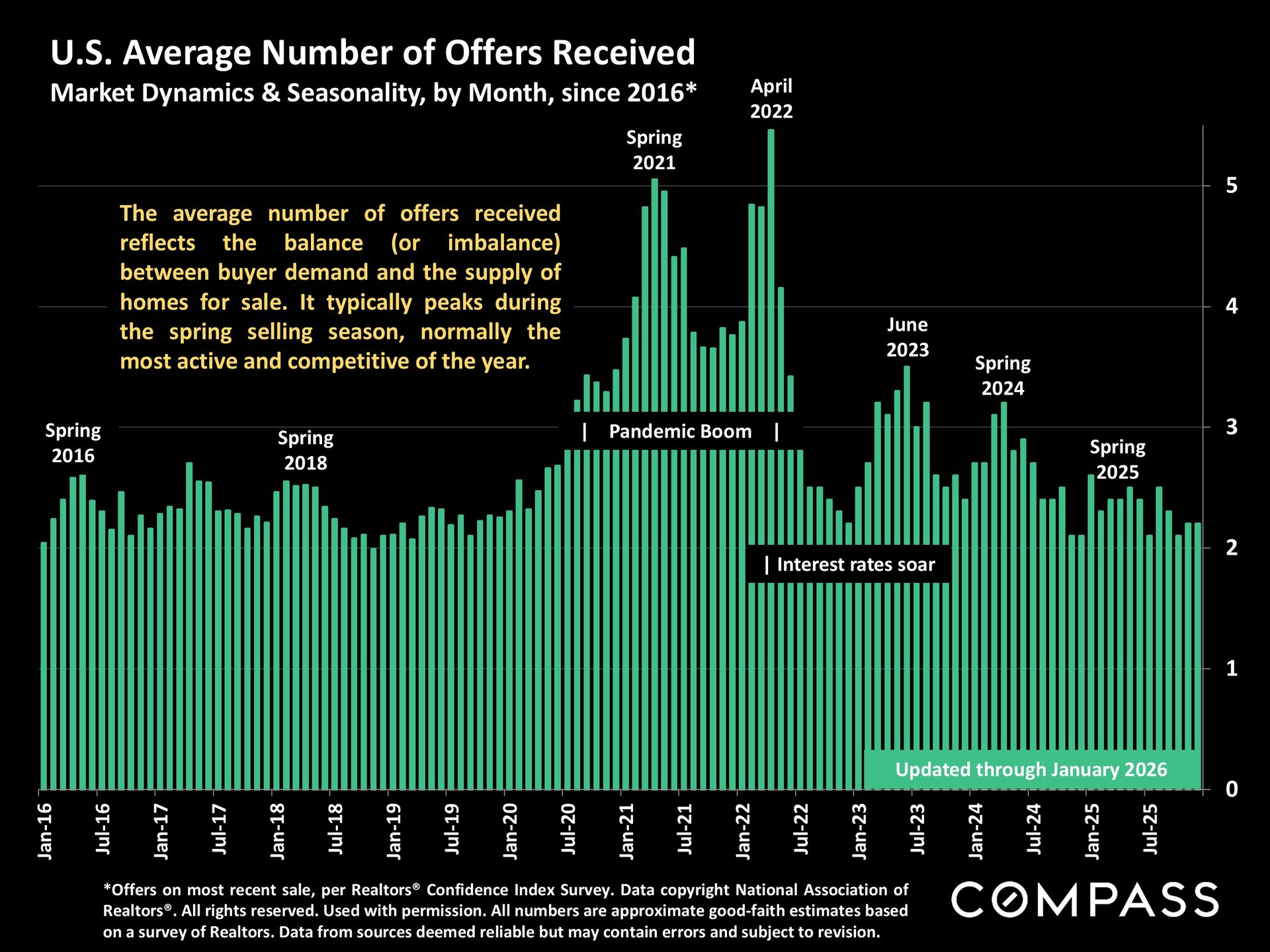

Average number of offers received: 2.2 (down from 2.6 last year)

-

Homes selling over list price: 16%

-

All-cash purchases: Estimated at 27% of sales

-

Vacation-home purchases: Approximately 3%

-

Contracts terminated before close (last 3 months): 5%

-

Delayed closings: 14%

These figures suggest a market that remains active but more measured than the highly competitive conditions seen in recent years. While multiple-offer scenarios are still common in certain segments, buyer urgency has moderated, and negotiation leverage is balancing out in many markets.

Photos Courtesy of Compass

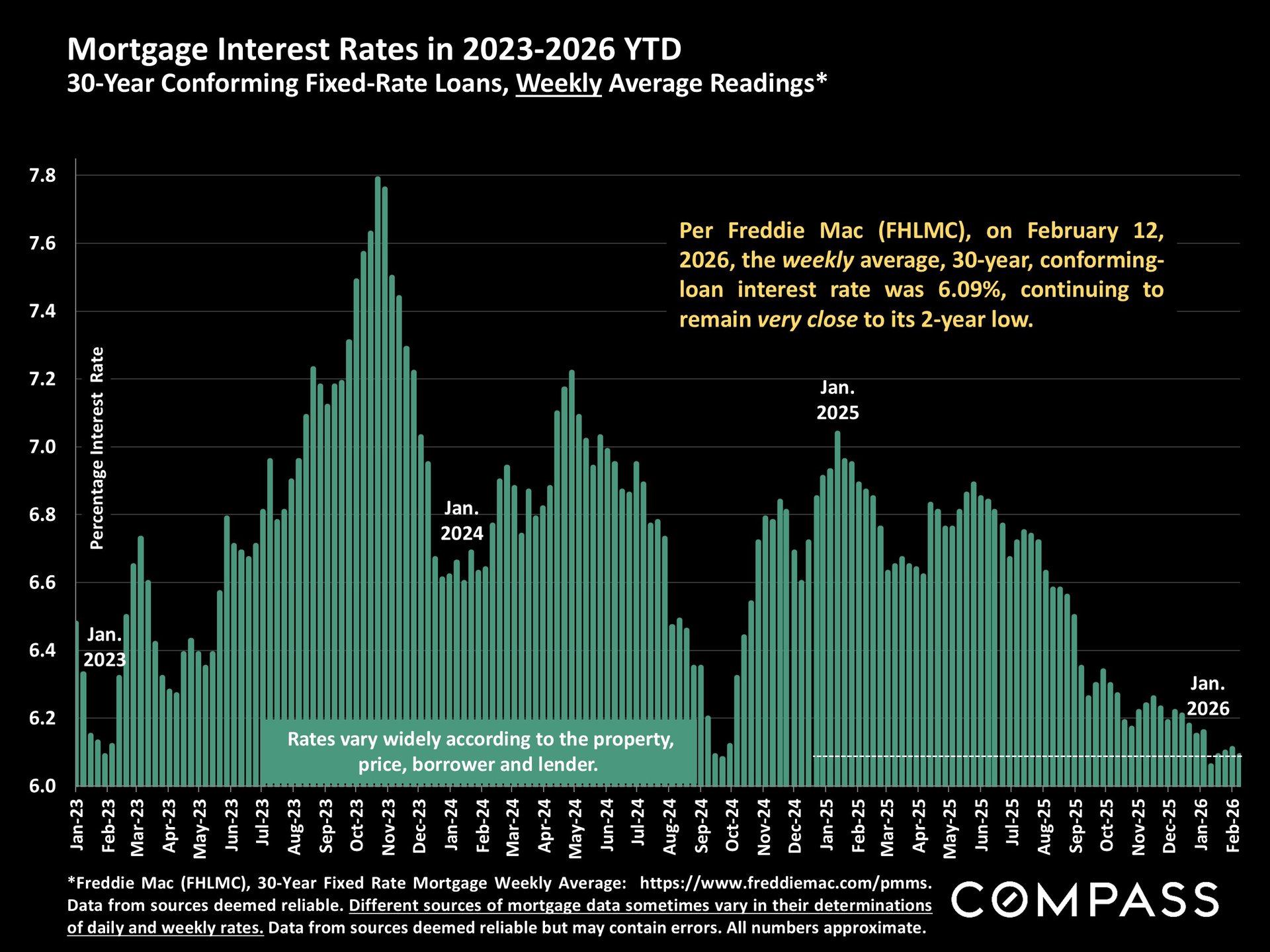

Economic Backdrop: A Mixed Picture

As of mid-February, interest rates remain near multi-year lows — a supportive factor for housing affordability and purchasing power.

However, broader economic signals are mixed:

-

Stock markets have experienced significant volatility, with both the S&P 500 and Nasdaq Composite pulling back from recent all-time highs. Dramatic daily swings have become common.

-

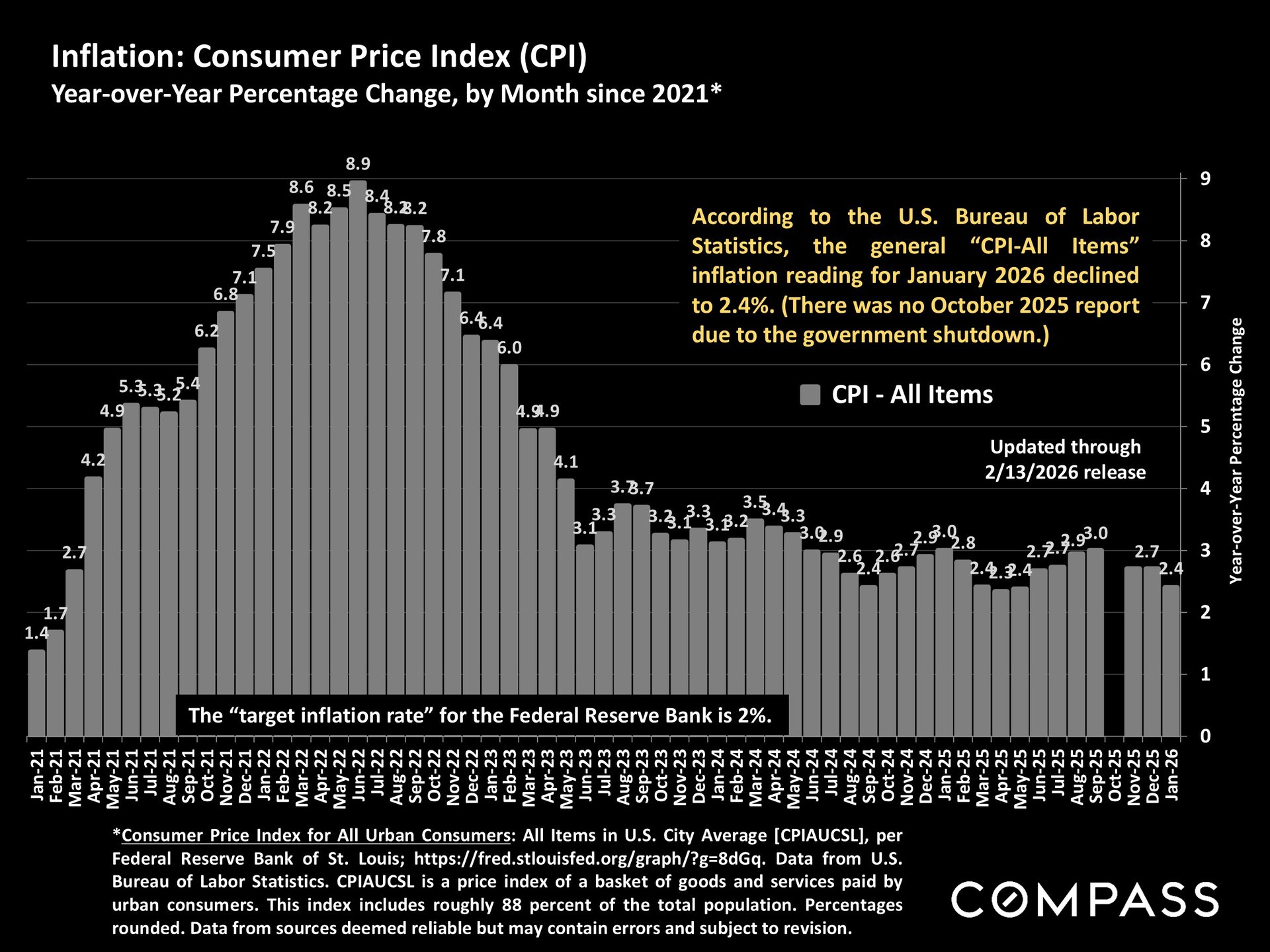

Inflation in January posted its best reading since May, an encouraging development.

-

Consumer confidence remains subdued amid ongoing concerns about prices and employment.

-

Net foreign immigration dropped sharply in the 12 months through July 1, 2025, and may turn negative in the current period, a shift that could have longer-term implications for housing demand in certain markets.

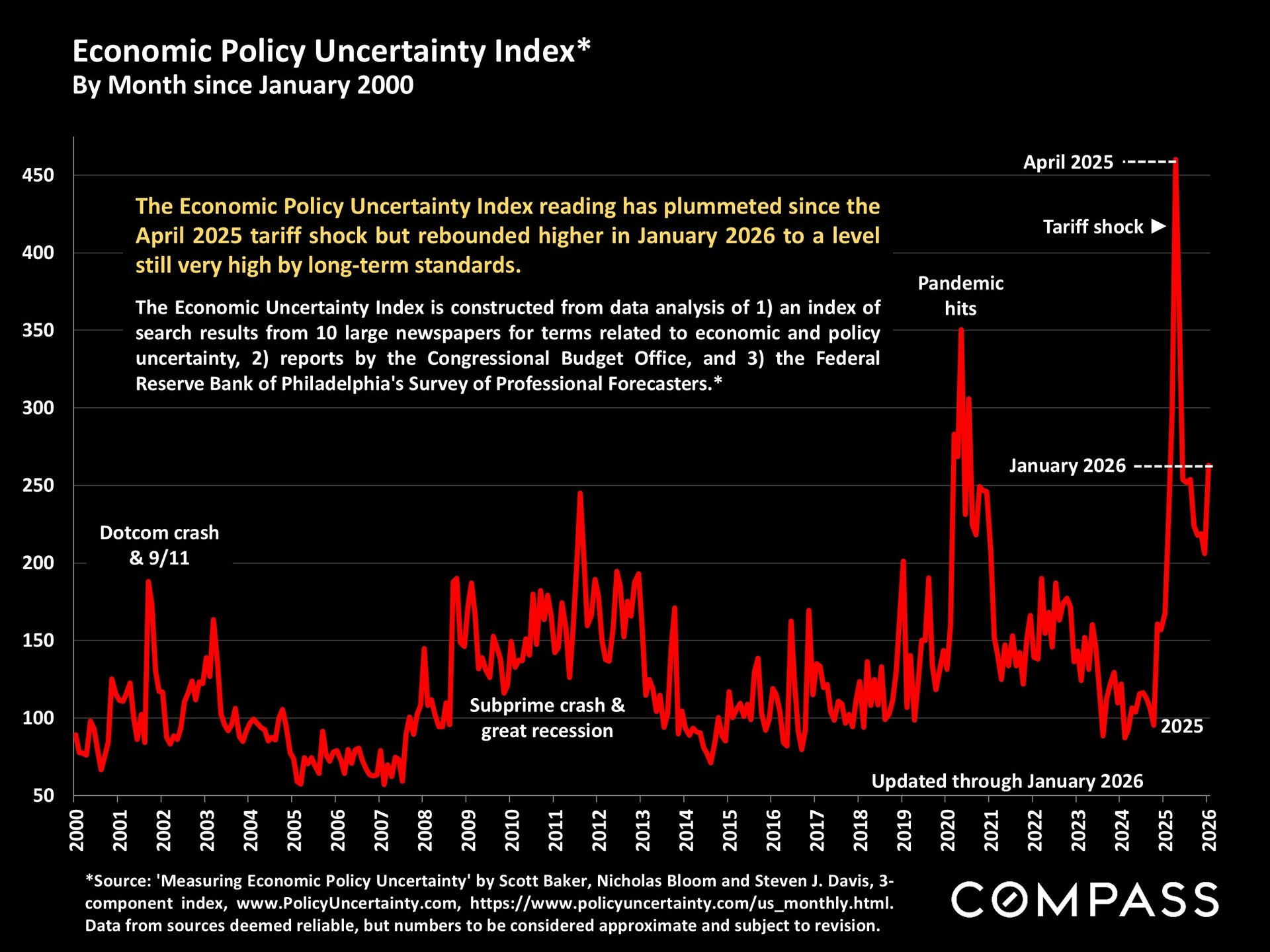

Taken together, these dynamics create a climate of cautious optimism. Lower rates are supportive, but consumer psychology remains sensitive to economic headlines.

What to Watch as We Move Toward Spring

The coming weeks will be critical. As new listings hit the market and buyer activity increases, we will gain much clearer insight into:

-

Whether demand rebounds strongly with improved weather and inventory

-

How sellers respond to slightly longer market times

-

Whether price growth accelerates or stabilizes

-

How economic volatility influences buyer behavior

Early signs point toward a healthier, more active spring compared to last year — assuming no unexpected economic shocks.

Photo Courtesy of Something Blue Photography

While national trends provide important context, real estate is always hyper-local. The real estate experts at The Blackshaw Messel Group are here to tailor these insights to individual markets and help you navigate what 2026 means for your specific goals.