The February 2025 real estate market followed predictable seasonal patterns, with the median sales price reflecting homes that went under contract in January. As expected, prices declined month-over-month but showed a notable 5% increase compared to February 2024. This continued year-over-year appreciation has significantly contributed to homeowner wealth but has made affordability a growing challenge, particularly for younger, less-affluent, and first-time buyers.

Homeownership as a Long-Term Investment

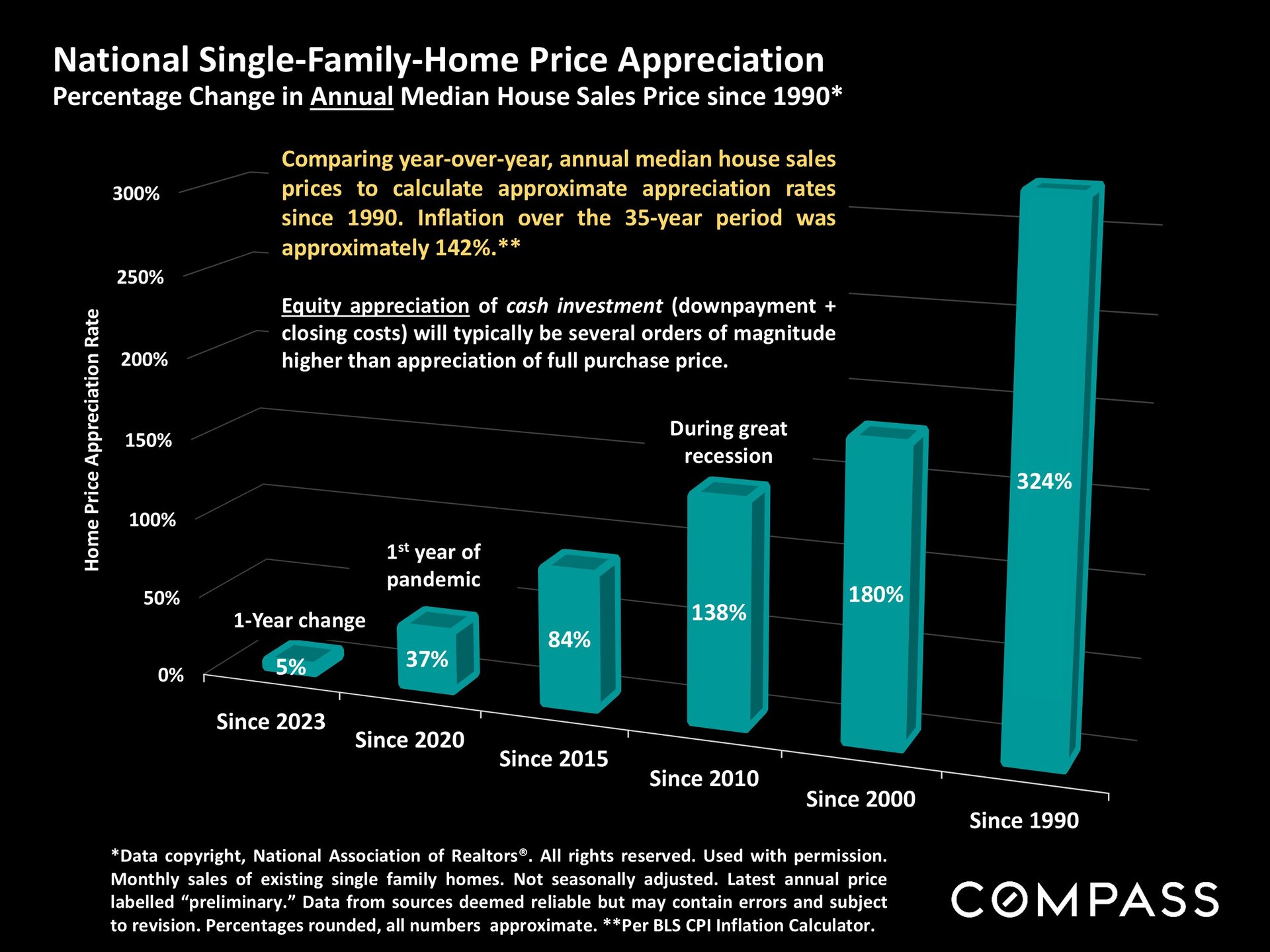

Despite affordability concerns, homeownership remains a historically strong investment. Looking at median house sales prices since 1990, real estate has consistently appreciated, offering both financial security and non-financial benefits, such as stability and community ties. Homeowners also enjoy tax advantages, including the $250K/$500K capital gains exclusion, which enhances long-term financial returns.

Photo Courtesy of Compass

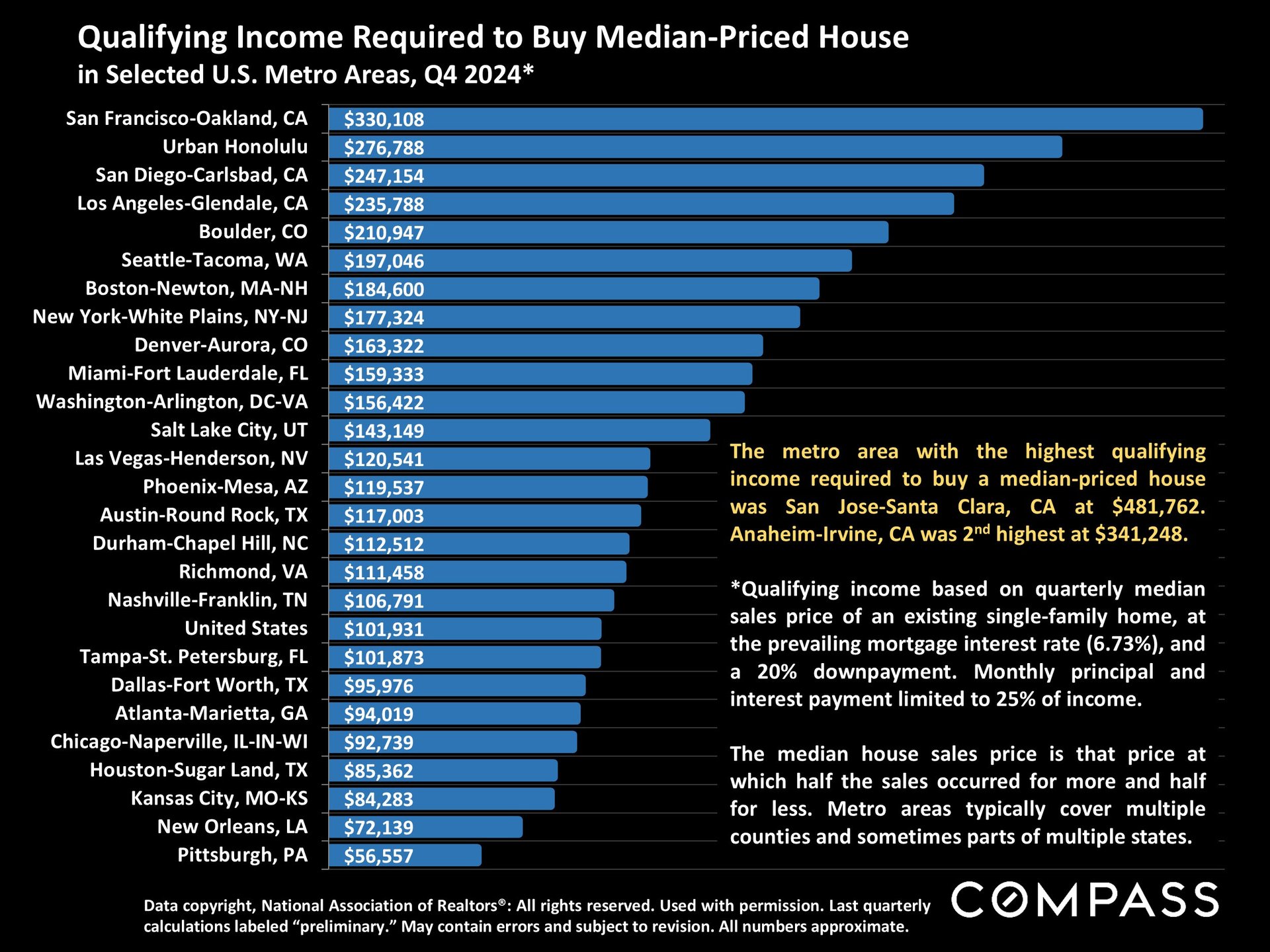

Qualifying Income & Market Affordability

A critical factor in homebuying is the income required to afford a median-priced home with a 20% downpayment. These figures vary widely across different U.S. metro areas, with affordability challenges becoming increasingly pronounced. The typical median home, featuring three bedrooms, two bathrooms, and 1,500 to 1,800 square feet, remains out of reach for many due to rising prices and interest rates.

Photo Courtesy of Compass

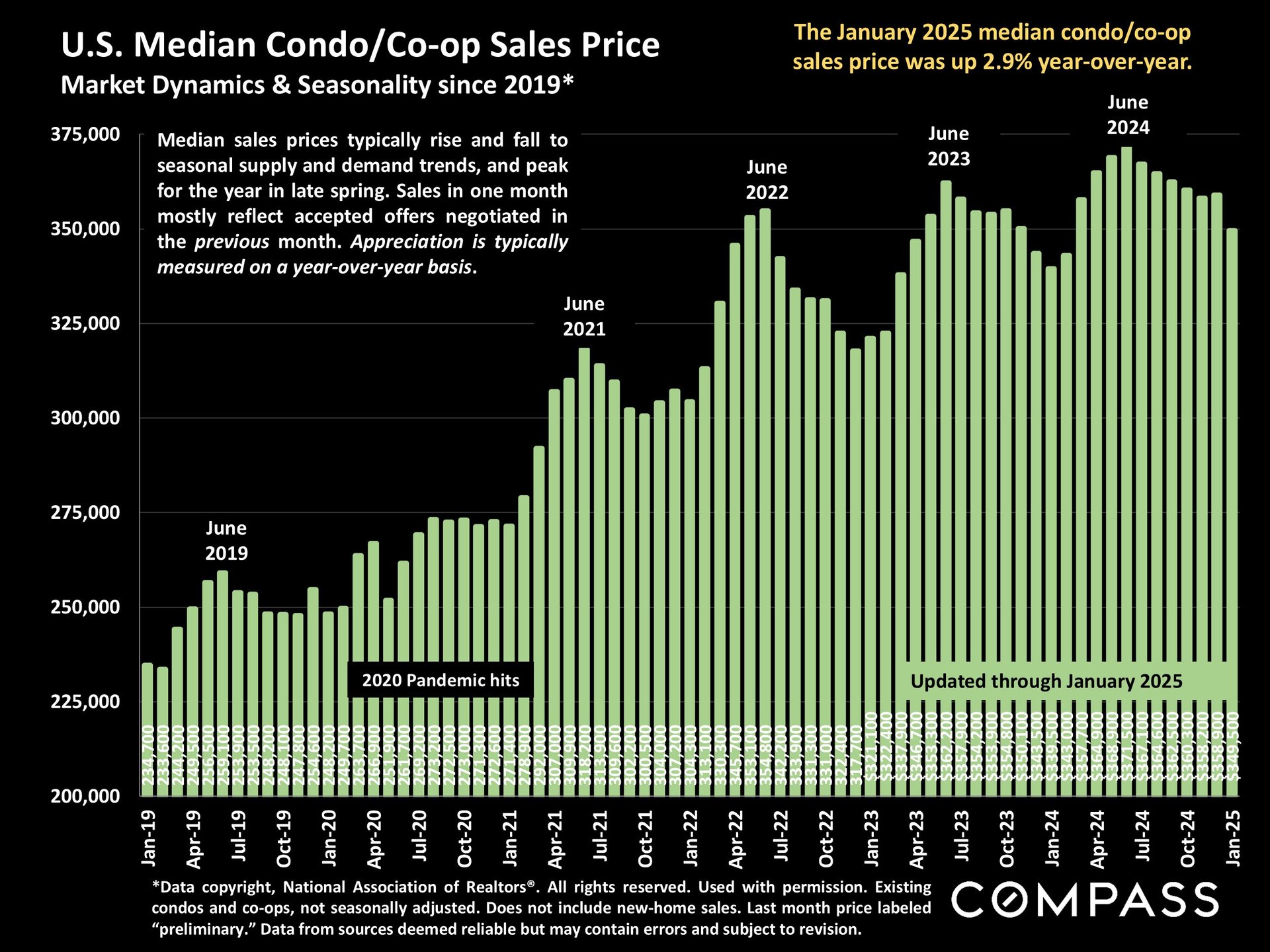

Trends in the Condo/Co-op Market

Market trends for condos and co-ops generally mirror those of single-family homes. These properties are most commonly found in urban centers and select vacation destinations. Like the broader market, condo/co-op sales follow seasonal patterns, with February reflecting the slowdown from January’s typical market dip.

Photo Courtesy of Compass

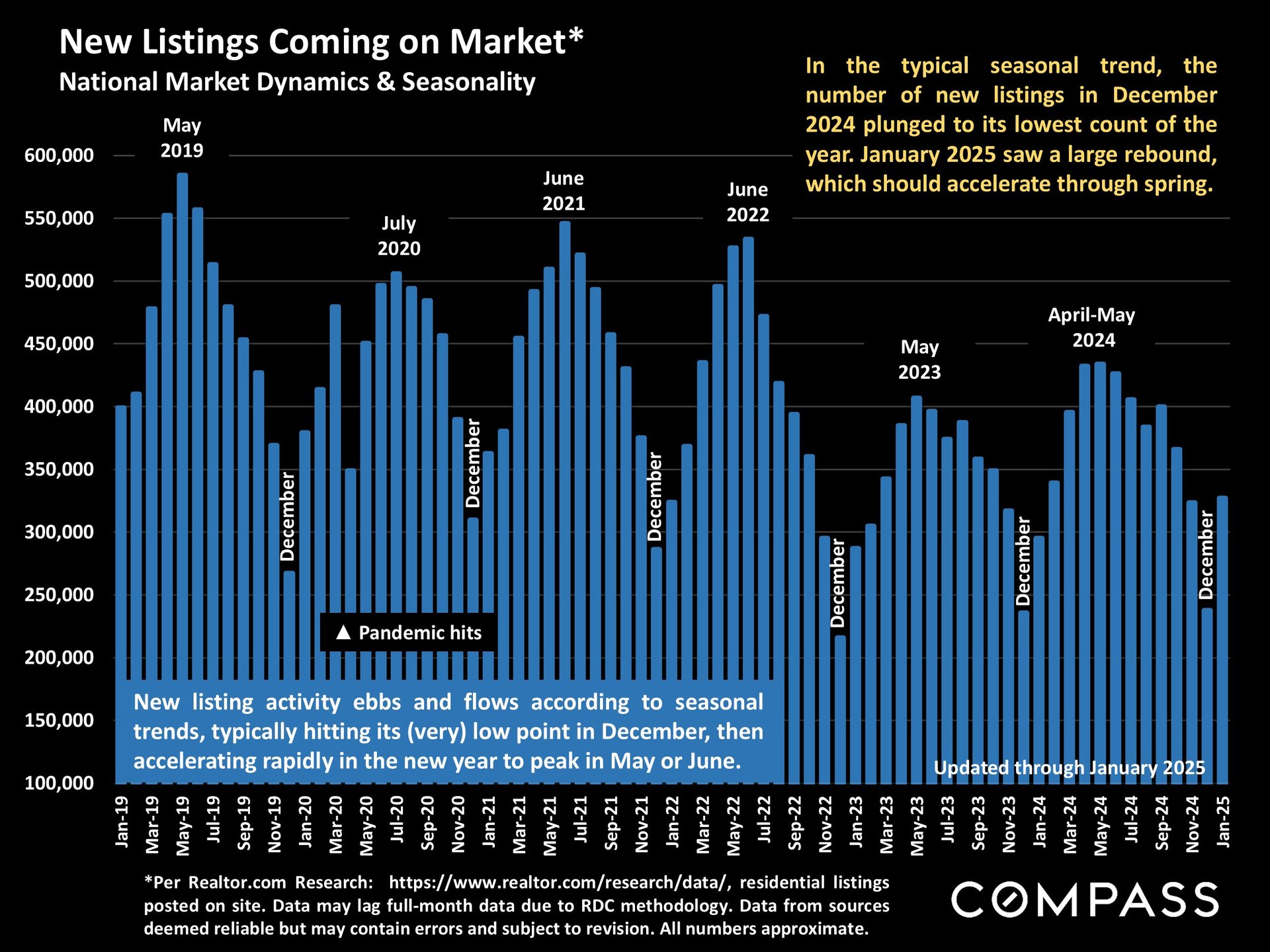

Seasonal Listing and Sales Volume Trends

New listings rebounded significantly in February, recovering from January’s seasonal low. This surge in listings is expected to accelerate through late spring, leading to increased closed sales in the coming months. Typically, January is the slowest market period, making February the nadir for closed transactions. However, with new inventory entering the market, activity is likely to increase substantially over the next four to five months, except in areas with distinct second-home market trends.

Photo Courtesy of Compass

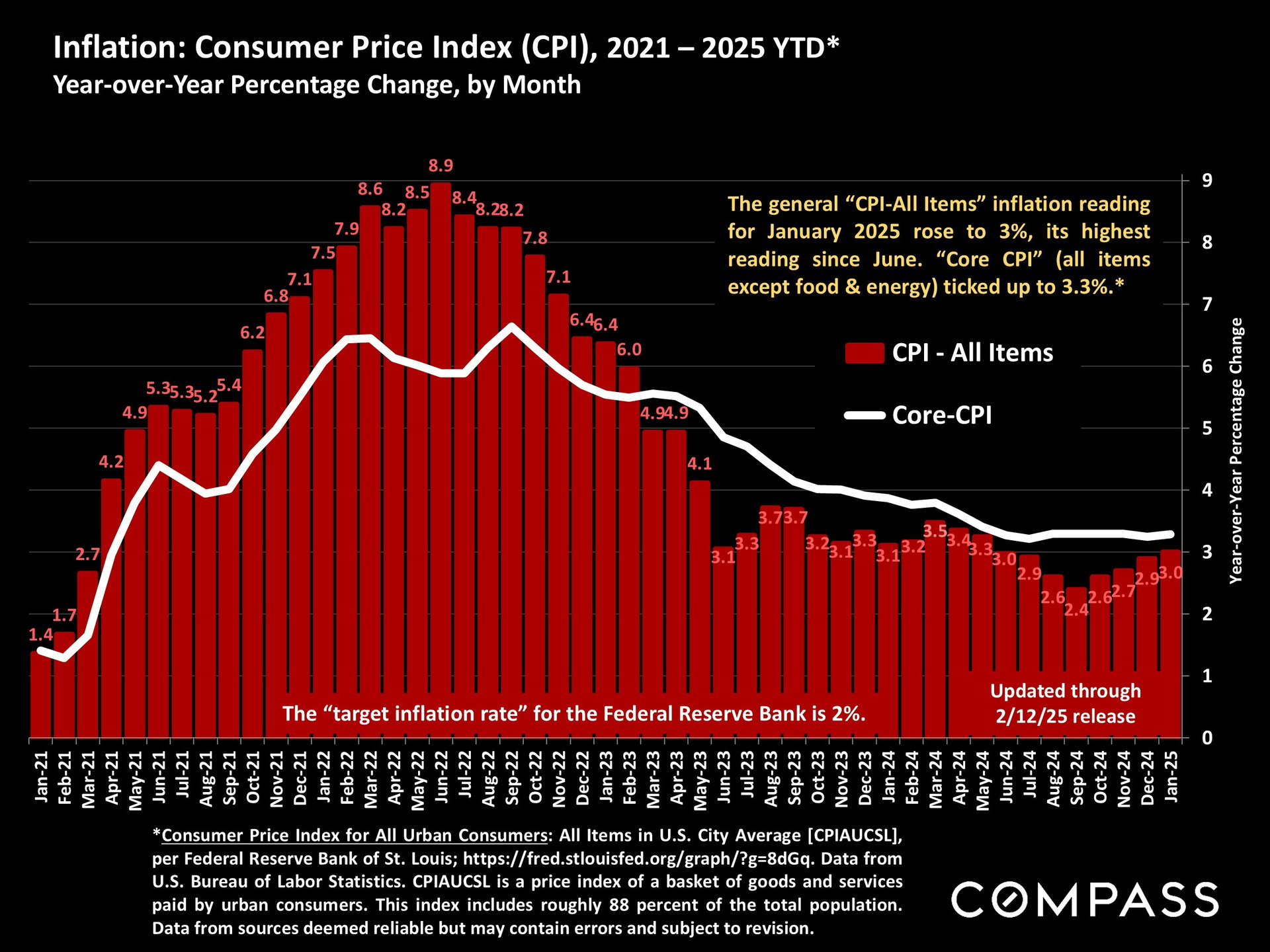

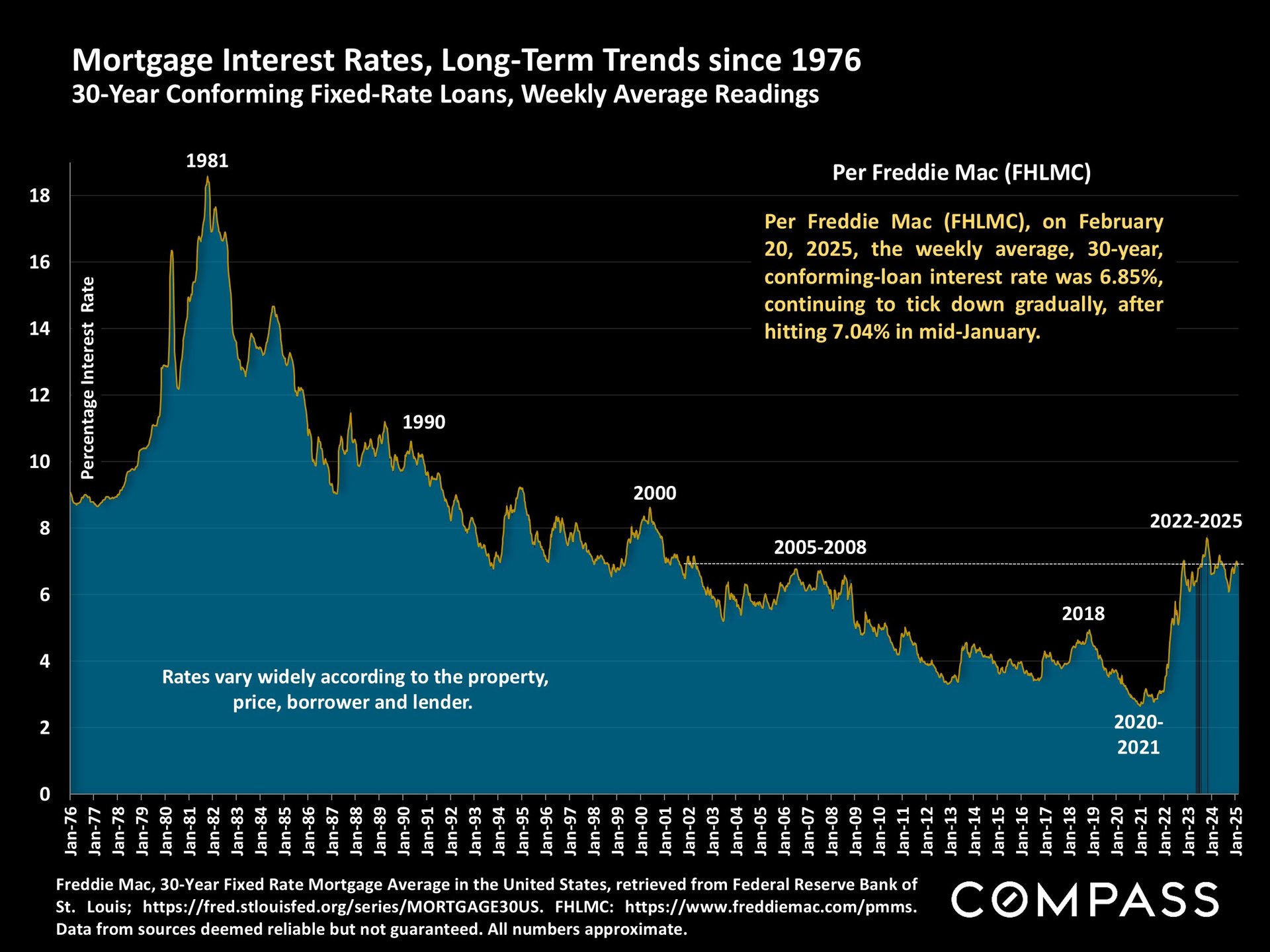

Interest Rates and Economic Influences

Interest rates play a crucial role in housing affordability. After ticking above 7% in February 2025, rates moderated slightly later in the month. While there was hope for rate cuts, the Federal Reserve remains cautious due to rising inflation, which has increased monthly since October 2024. Additionally, new and proposed tariffs add uncertainty regarding their potential impact on inflation, interest rates, and construction costs.

Photo Courtesy of Compass

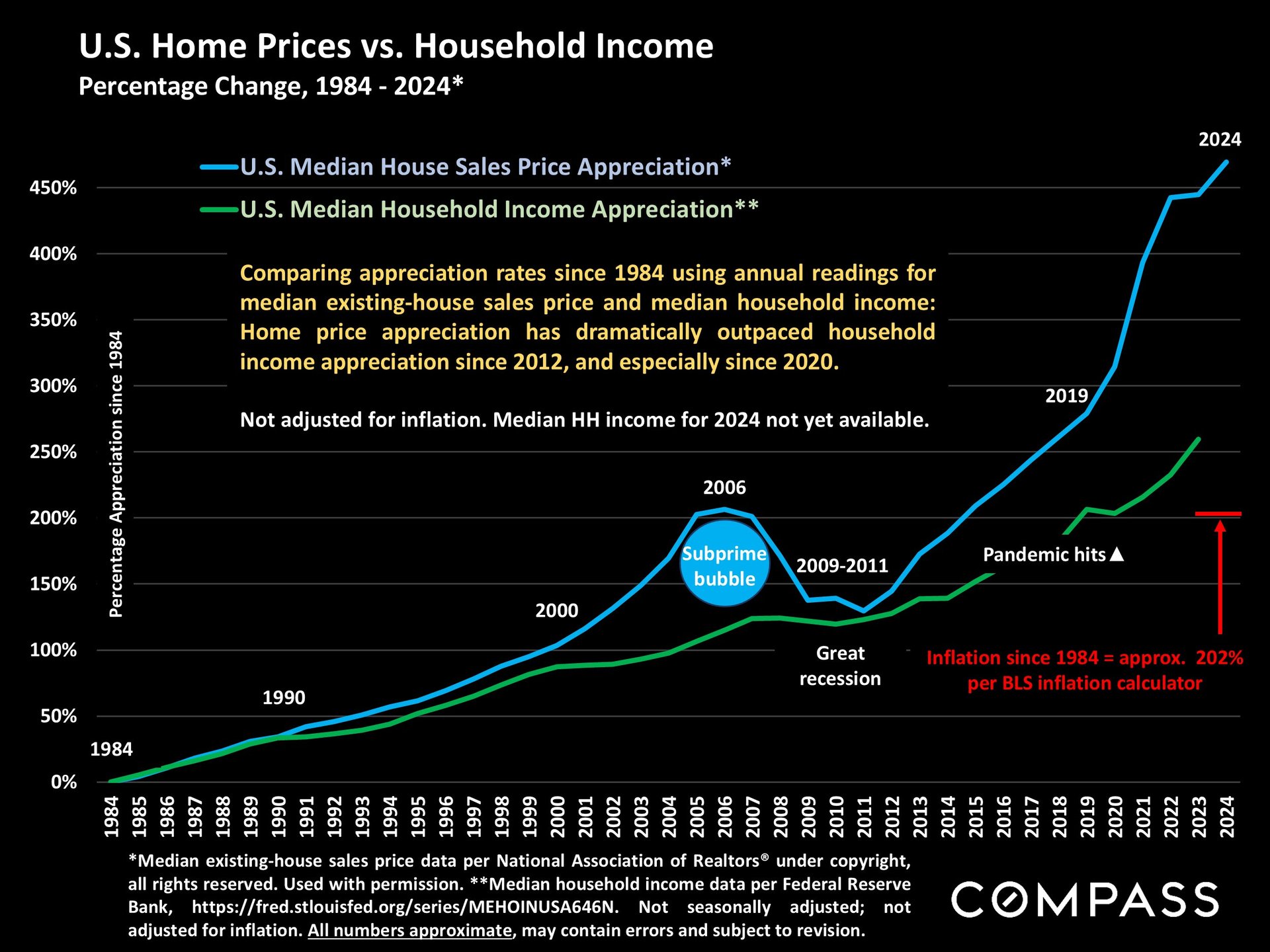

Home Prices vs. Household Income Growth

One of the most pressing concerns in the housing market is the widening gap between home price appreciation and household income growth. Since 2012—and particularly post-2020—home prices have outpaced incomes, making homeownership increasingly difficult for younger generations. This shift has skewed home sales toward older, wealthier buyers, who tend to move less frequently, thereby limiting new listings and further tightening supply.

Photo Courtesy of Compass

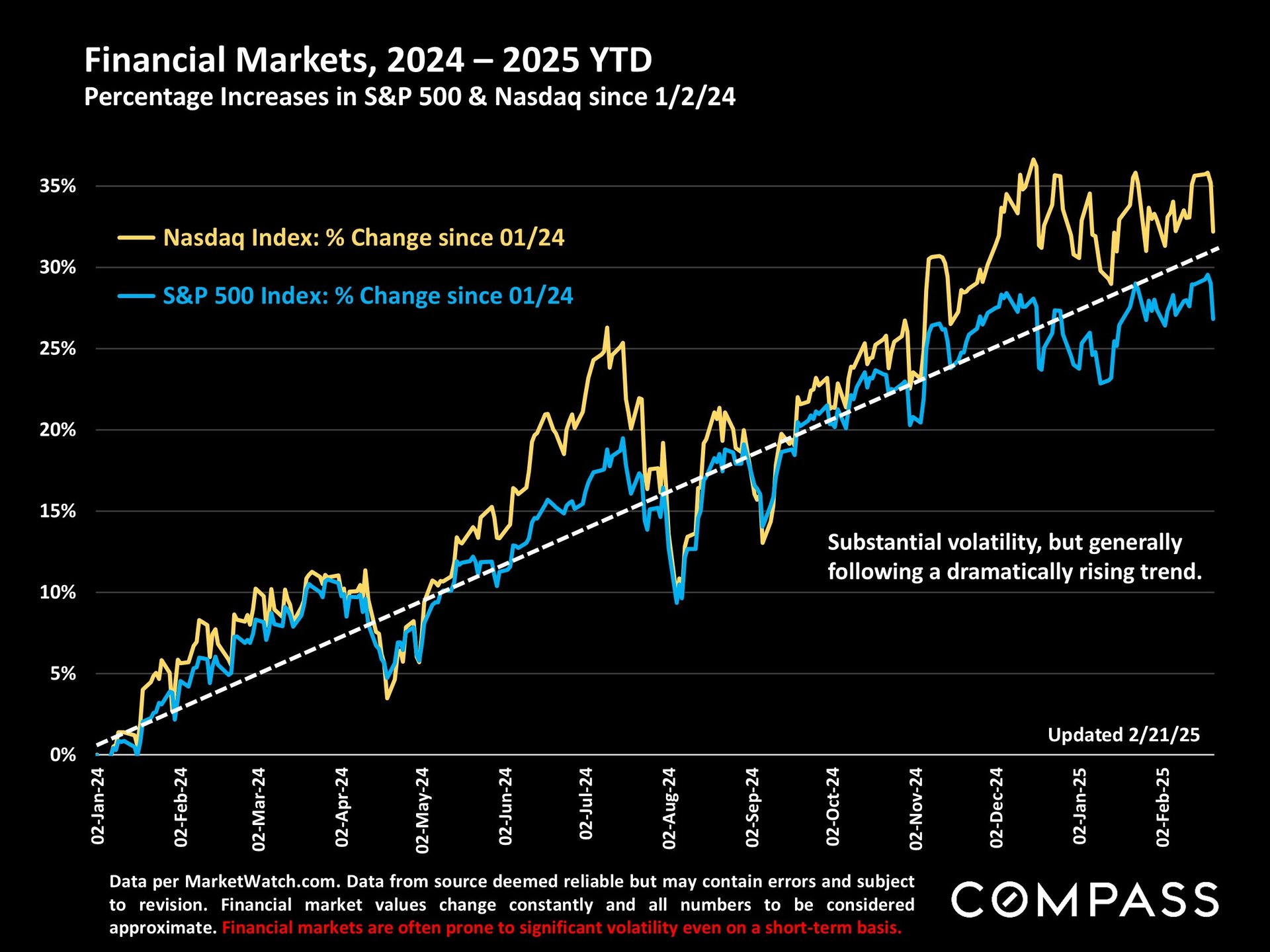

The Impact of Stock Market Growth on Housing

With stock markets experiencing substantial gains over the past 14 months, household wealth has increased for those invested in financial assets. This has led to a rise in all-cash home purchases, reducing sensitivity to mortgage interest rate fluctuations and further increasing competition in the housing market.

Photo Courtesy of Compass

New Construction & Inventory Challenges

Despite a low number of resale home listings relative to long-term norms, the inventory of new-construction homes has surged to its highest level since 2008. States like Texas, Florida, and North Carolina are seeing the most significant new development, with new homes making up a growing share of total sales.

Photo Courtesy of Compass

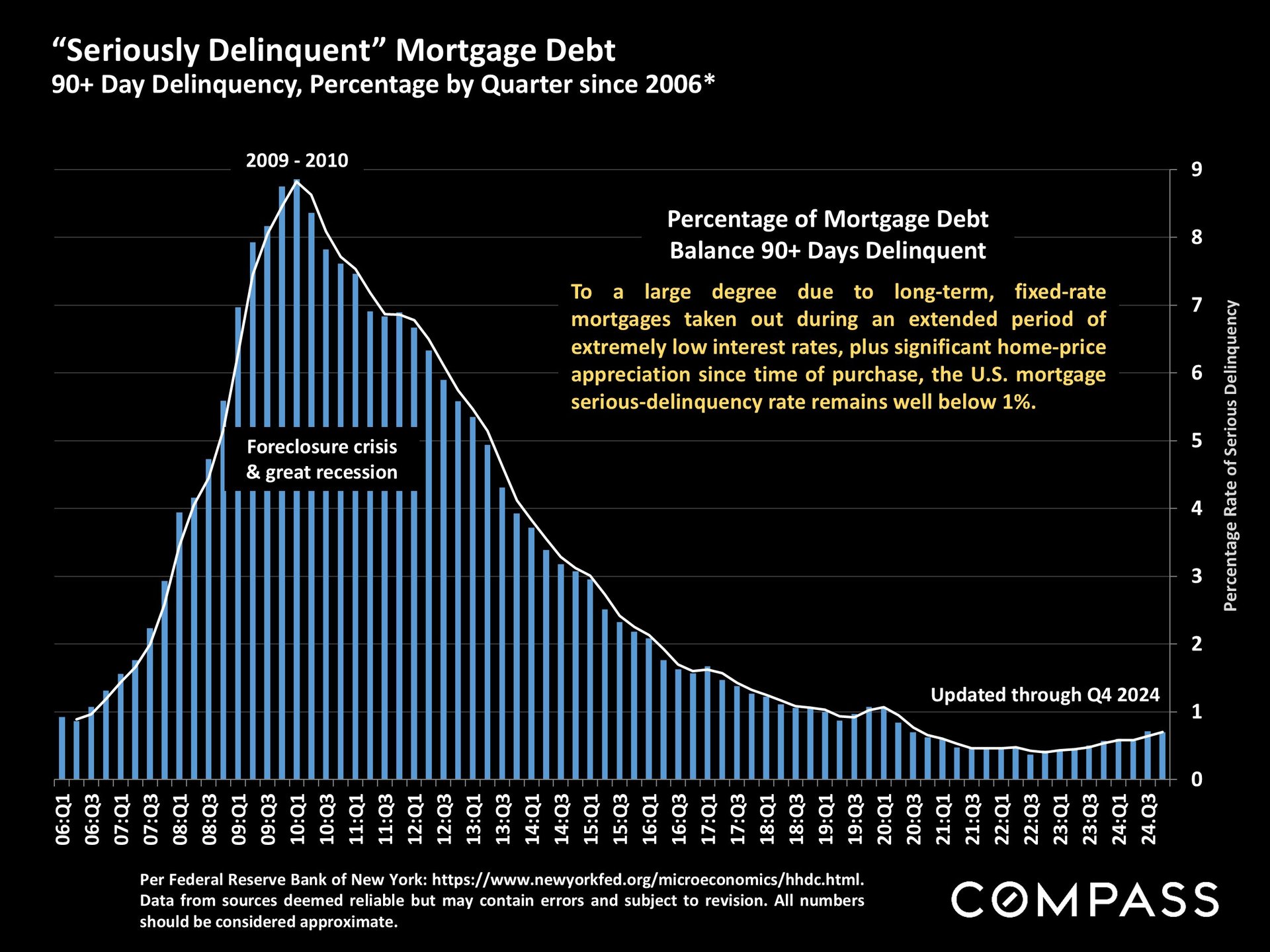

Mortgage & Credit Card Delinquencies

Although credit card delinquencies (90+ days overdue) have reached their highest levels since 2012, mortgage delinquencies remain near historic lows. Thanks to rising home prices and the prevalence of long-term, fixed-rate loans, homeowners are generally in a stable financial position, reducing the risk of widespread mortgage distress.

Photo Courtesy of Compass

Looking Ahead

As the real estate market moves into the busiest season of the year, key factors to watch include:

-

The trajectory of interest rates and Federal Reserve policy decisions.

-

The impact of inflation and potential tariff changes on construction costs.

-

The continued challenge of affordability, particularly for first-time buyers.

-

Inventory trends, with new-construction homes playing an increasingly vital role in housing supply.

With the spring market approaching, buyers and sellers alike should stay informed and work with experienced professionals to navigate the evolving landscape. If you're considering buying or selling, reach out to The Blackshaw Messel Group for expert guidance tailored to your needs.